Martino Grasselli, Coordinateur du Laboratoire de recherche en finance De Vinci Finance Lab, rend disponible son article de recherche « The 4/2 Stochastic Volatility Model » sur le réseau SSRN (Social Science Research Network).

Ce papier de recherche à notamment été présenté au QMF 2013 à Sydney.

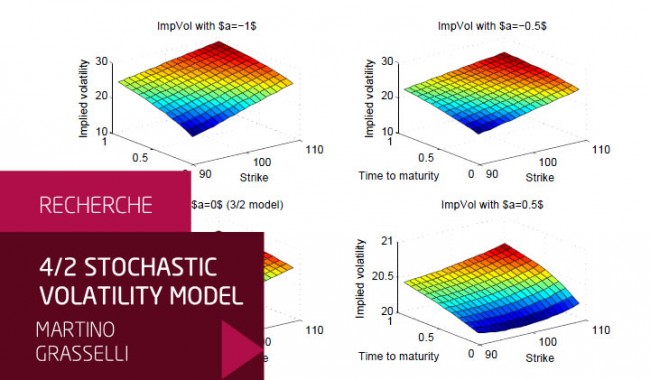

Abstract

We introduce a new stochastic volatility model that includes as special cases the Heston (1993) and the 3/2 model of Heston (1997) and Platen (1997). The new model displays new features, namely the instantaneous volatility can be uniformly bounded away from zero, and it is highly tractable, meaning that the pricing procedure can be performed efficiently. This required the application of the Lie symmetries theory for PDEs, which allowed us to extend known results on Bessel processes. Finally, we provide an exact simulation and a second order discretization scheme for the model, which is useful in view of the numerical applications.

Keywords: Stochastic volatility; Volatility modelling; Lie’s symmetries; Laplace Transform; Exact Simulation.

Télécharger l’article sur SSRN